Safeguarding Against Section 43B Disallowances for MSME Suppliers in the Income-Tax Act

In India’s intricate tax landscape, laying the groundwork for diligent compliance can be challenging, especially with specific requirements relating to Micro, Small, and Medium Enterprises (MSMEs). Section 43B of the Income-tax Act, a provision aimed at certain deductions at the point of payment, plays a pivotal role in this scenario, particularly for assesses dealing with MSME suppliers.

While the statute helps maintain barriers against potential fiscal evasion, it necessitates a stringent adherence from MSME suppliers to their documentation process, reflecting their verified status. This documentation is not only crucial for maintaining transparency but also dramatically influences the operations of MSME suppliers and their interaction with various stakeholders.

Clarifying MSME Status & Legal Requirements

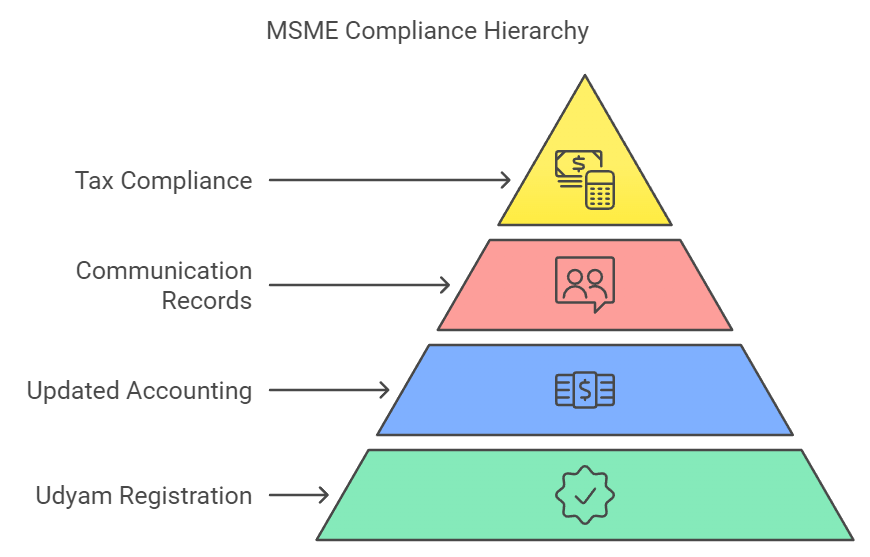

In today’s dynamic business environment, a vital initial step for the assesse involves obtaining a declaration of the supplier’s MSME status, invariably accompanied by the Udyam registration certificate.

This certificate, which validates an enterprise’s recognition under the central government’s Udyam Registration scheme, helps define the nature of the inter-firm relationship – an aspect that bears significant implications under the broader tax regime. For this registration process and to understand how it benefits your business, you can refer to this excellent guide on business registrations.

No less important is the necessity to keep the accounting software updated with the supplier’s master data. Such data helps identify the composite engagements with suppliers and serves as a source of validation for the supplier’s MSME status, thereby enhancing the accountability of transactions and aiding in effective decision-making.

Yet, what if you encounter situations where, despite concerted efforts, no communication regarding the MSME status is received from the supplier? In such scenarios, retaining a copy of the necessary communication with the supplier fortifies the documentation.

Notably, if such circumstances arise, both Sections 15 of the MSMED Act and Section 43B of the IT Act will not apply. More, it emphasizes the proactive role of an assesse in maintaining clear channels of communication and ensures an added layer of protection in their tax compliance journey.

Supplier Relationships & Payment Terms

Within the ambit of India’s robust legal framework, specifically, the MSME Development (MSMED) Act, Section 15 holds a place of prominence. It mandates the payment to MSME suppliers within a stipulated timeframe. Not only does this protect the financial interests of MSMEs, but it also prompts businesses to implement transparent and efficient payment processes.

To achieve a seamless execution of these obligations, clear payment terms need to be meticulously defined and embedded within every purchase order. These terms, potentially varying transaction-wise, should be specifically stated to avoid discrepancies and foster a sense of reliability and trust between the trading entities.

Moreover, incorporating a feature within the accounting software that can proactively manage due date reminders for each transaction individually is imperative. This technological integration ensures that the payment obligations are met in a timely manner, thereby strengthening adherence to the compliance norms set forth by the MSME Development Act.

Addressing the innate complexities within inter-firm trade dynamics, especially in the context of the Income-tax provisions, requires a concerted focus on managerial and operational nuances. It’s essential to marshal through these challenges, tethered by an unwavering commitment to statutory compliance and optimized supplier relations. Businesses must regard these legal stipulations not as hurdles but as integral components of their operational excellence.

For an exhaustive understanding of how income tax provisions impact your business strategies and supplier relationships, consultation with seasoned tax experts who offer comprehensive income tax services can be invaluable.

Managing Objections and Ensuring Quality

Prompt and effective management of objections is as much a part of quality assurance as it is of financial compliance. A crucial practice that remains a cornerstone in dealings with MSME suppliers is the immediate addressal of any defects in goods or deficiencies in services.

To legalize the objection, it must be put in writing within 15 days of the detection. While these objections play a pivotal role in nurturing continuous improvement and maintaining quality benchmarks, they also have significant implications for MSME-related tax compliance.

Recording the objection date and the subsequent resolution by the vendor determines the onset of the payment timeframe. It is from this date that the clock begins to tick on the countdown to the payment due date in accordance with the MSME Act.

Therefore, maintaining an accurate and detailed record system for such communications is not only a best practice but also a legal requirement, aligning with the broader objective of establishing an unambiguous timeline for financial due diligence.

Finance Narratives in a New Age: Implications of General Remarks on MSME Status in Financial Statements

Navigating through the evolving financial documentation landscape, a practice that has garnered attention is the inclusion of general remarks regarding the lack of information on MSME status of suppliers in financial statements and tax audit reports.

The Guidance Note on Tax Audit under section 44AB of the Income-tax Act, 2022, recommends tax auditors to make such a disclosure. However, this approach might be on the brink of a significant shift.

Businesses today must recognize that the tolerance for ambiguity in financial reporting is rapidly diminishing. Regulatory bodies are placing a sharper focus on the substantiation of claims and disclosures made in financial documents.

In the context of MSME status, the lack of specific information could potentially pave the way for tax authorities to raise objections and enforce disallowances under section 43B of the Income-tax Act. The prospective line of inquiry from the department regarding the MSME status of creditors underscores the need for a more rigorous and transparent reporting approach.

Therefore, it is of paramount importance that businesses re-evaluate their current practices. Ensuring that the financial statements reflect precise details on the MSME status of suppliers could very well be a requisite to safeguard against future tax liabilities and penalties.

Potential Consequences without Verified MSME Status Information

Having accurate information on the MSME status of suppliers isn’t just a good-to-have feature—it’s an essential cog in the wheel of financial compliance. A lapse in verifying this status can lead to severe repercussions, including financial disallowances.

Under Section 43B of the Income-tax Act, such disallowances might be made if the required payments to MSMEs are not fulfilled within the specified time. This measure is designed to ensure that MSMEs, which often operate with limited financial buffers, aren’t left in precarious positions due to delayed payments.

The necessity of maintaining accurately verified MSME status information thus becomes clear. Non-verifiable information or misrepresentation can entail tax authorities disputing the claims, leading to tax liabilities and considerable fines. This stipulation elevates the need for strict adherence to the MSME Act and a structured documentation process that can effectively stand the scrutiny of tax audits.

Ensuring Compliance with the MSMED Act

Compliance with Sections 16, 22, and 23 of the MSMED Act carries its own set of obligations, which are essential to uphold for any business engaged with MSME suppliers. These sections encompass the furnishing of details regarding unpaid amounts, the buyer’s liability when payment is delayed, and the interest provision due on outstanding amounts to MSMEs. Depending on the jurisdiction, businesses must navigate these sections diligently to ensure that all legal mandates are met without a shortfall.

To maneuver through these requirements, businesses need to have systematic processes and an up-to-date understanding of the MSMED Act. It’s recommended that businesses seek professional guidance to manage these legal encumbrances.

This is not just about following regulations but also about supporting the MSME sector, which is often hailed as the backbone of the Indian economy. Compliance, in this regard, demonstrates a company’s commitment to responsible corporate governance.

Conclusion

Throughout this article, we have explored the intricate nuances that govern financial interactions with MSME suppliers within the context of the Income-tax Act and MSMED Act. We’ve established the paramount importance of adhering to the legal requirements for verifying MSME status and the need for robust documentation processes to ensure seamless compliance.

By taking proactive steps—such as acquiring the Udyam registration certificate, maintaining detailed supplier communications, setting explicit payment terms, and comprehensively managing quality objections—businesses can fortify their position against the potential disallowances under section 43B of the Income-tax Act.

Remaining vigilant about the compliance with Sections 16, 22, and 23 of the MSMED Act further ensures that businesses honor their obligations and support the continued vitality of the MSME sector, a critical driver of the nation’s economic engine.

In conclusion, the need to remain scrupulously compliant within the ambit of India’s financial regulations cannot be overstated. While navigating the complexities of these statutory requirements may seem daunting, it is a journey that reaps rewards not only in terms of regulatory compliance but also in building enduring, trustworthy relations with the MSME community. It is, by all means, a worthwhile endeavor that underscores the spirit of both legal fidelity and ethical business practice.

Disclaimer

The materials provided herein are solely for educational and informational purposes. No attorney/professional-client relationship is created when you access or use the site or the materials. The information presented on this site does not constitute legal or professional advice and should not be relied upon for such purposes or used as a substitute for professional or legal advice.